northcell › blog › sinking funds

Sinking Funds vs Emergency Funds: What's the Difference?

A sinking fund is money you set aside on purpose for something you know is coming. An emergency fund is money you keep ready for something you cannot predict. One spring, two things went wrong in the same week. The car needed new brakes, and our water heater quit. One of those I had been quietly saving for. The other I had not. Watching how differently those two bills felt is the clearest way I know to explain the difference between a sinking fund and an emergency fund.

People mix these two up all the time, and it costs them, because the fix for one is not the fix for the other. Here is the clean line between them, when you reach for which, which to build first, and how to run them both without turning your bank into a spreadsheet of its own.

Key takeaways

- A sinking fund is for expenses you can see coming. An emergency fund is for the ones you cannot.

- You want both. They do different jobs, and keeping them separate is what stops you from raiding your emergency fund for the holidays.

- A common order: build a small starter emergency fund first, then add sinking funds for known bills, then grow the emergency fund to a fuller cushion.

- You do not need separate bank accounts. You need each balance tracked separately so the money does not blur into one pile.

The one-sentence difference

A sinking fund is money you set aside on purpose for something you know is coming. An emergency fund is money you keep ready for something you cannot predict. Planned versus unplanned. That is the whole distinction, and almost every other difference follows from it.

| Sinking fund | Emergency fund | |

|---|---|---|

| What it is for | A known, planned expense with a date | An unexpected, unplanned shock |

| Examples | Car insurance, holidays, registration, vacation, new tires | Job loss, surprise medical bill, an urgent home repair |

| When you use it | On a schedule you already know | Rarely, and never on purpose |

| How you fund it | Divide the total by the months until it is due, set that aside monthly | Build steadily toward a months-of-expenses cushion, then leave it alone |

| How many you have | Several, one per category that has hurt you | Usually just one |

| If you skip it | A predictable bill becomes a credit-card surprise | A real emergency turns into debt |

What a sinking fund is

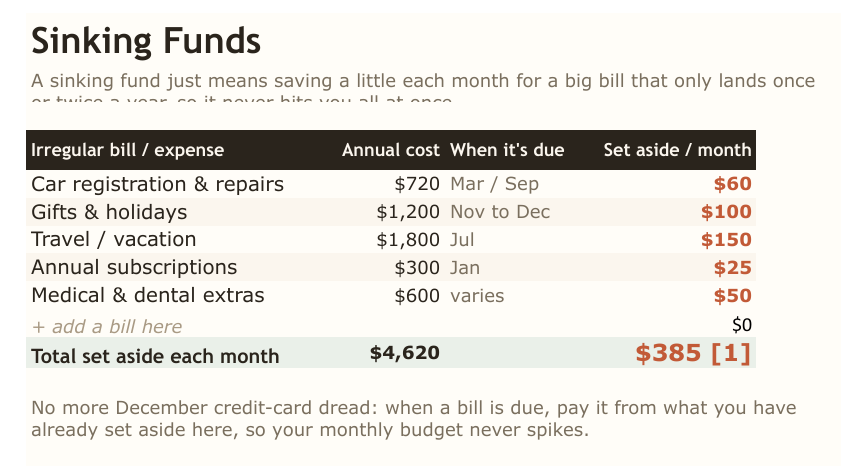

A sinking fund is just deciding ahead of time. You take an expense you know is coming, divide it into small monthly amounts, and set that money aside until the bill shows up. The car insurance that lands as one big hit in March becomes a calm monthly number you barely notice. If you want the full list of which categories are worth having and how much to set aside for each, I wrote that up here: sinking fund categories, with real examples.

What an emergency fund is

An emergency fund is protection, not a plan. It is the cushion that absorbs the genuine surprises so they do not turn into debt: the layoff, the ER visit, the thing you truly did not see coming. You build it up over time and then you mostly leave it sitting there, a little boring, doing its quiet job of letting you breathe when life lurches.

Why you want both

Here is the trap I watched people fall into, and fell into myself early on. If you only have an emergency fund, every predictable bill, the holidays, the insurance, the registration, ends up raiding it. Then a real emergency arrives and the cushion is half gone, spent on Christmas. The two funds protect each other. Sinking funds keep the planned costs from ever touching the emergency fund, and the emergency fund stays whole for what it is actually for.

Which should you build first?

A common and sensible order looks like this. Start with a small starter emergency fund, enough that a true surprise does not knock you flat. Then layer in sinking funds for the irregular bills you know are coming, because those are what otherwise wreck a budget month to month. Then, with the predictable stuff handled, grow the emergency fund to a fuller cushion of several months of essential expenses. The exact order depends on your life, but having a little of both early beats having a mountain of only one. This is how I think about it, not a rule for your situation.

How to keep them separate without ten bank accounts

You do not need a bank account for every fund. That is a tidy idea that quietly becomes a chore. What you actually need is one place that shows each balance on its own line, so your holiday fund, your car fund, and your emergency fund stay clearly separate even if the dollars live in the same account. Tracking is what does the real work here, not the number of accounts. This is the part the free starter sheet handles for you: you list each fund, and it keeps every balance growing on its own.

free download

Get the free Sinking Funds Tracker

I built a free starter version of the exact sheet I use with my own family. You list your planned bills, it works out the small amount to set aside each month, and it tracks every balance separately so nothing sneaks up on you. Tell me where to send it and it is yours.

When you want it wired into your whole year

The free tracker covers your sinking funds. If you want them flowing straight into a budget that also forecasts which months will run tight and shows your whole year at once, that is what the northcell Annual Budget does. The sinking-fund set-asides live right alongside a full 12-month dashboard, so the planned bills and the rest of your money sit in one calm view.

Frequently asked questions

What is the difference between a sinking fund and an emergency fund?

A sinking fund is money you set aside on purpose for an expense you know is coming, like car insurance or the holidays. An emergency fund is money you keep for the expenses you cannot see coming, like a job loss or a surprise medical bill. One is planned, the other is protection.

Which should I build first, a sinking fund or an emergency fund?

A common approach is to build a small starter emergency fund first so a true surprise does not knock you over, then add sinking funds for your known irregular bills, then grow the emergency fund to a fuller cushion over time. The right order depends on your situation, but having a little of both early beats having a lot of only one.

Can I keep my sinking funds and emergency fund in the same account?

Yes. You do not need a separate bank account for each one. What you need is to track each balance separately so the money does not blur into one pile you dip into without noticing. A simple tracker does this better than ten bank accounts.

Is a sinking fund the same as savings?

It is a specific kind of savings. Regular savings can be vague, money you are keeping for someday. A sinking fund has a job: a named expense, a target amount, and a date, so you know exactly when it will be spent and on what.

How much should I keep in an emergency fund?

A widely used guideline is three to six months of essential expenses, built up over time, with a smaller starter amount first. The right number depends on how stable your income is and how many people depend on it. This is general education, not advice for your situation.

Related reading

Designed and written by northcell. For organization and planning purposes only, not financial, tax, or legal advice. Our tools and guides are original works created with AI-assisted design; every formula is human-tested and verified.