northcell › blog › sinking funds

Sinking Fund Categories: Real Examples (and How Much to Set Aside for Each)

A sinking fund is money you set aside a little at a time for a known, planned expense (like car insurance or the holidays), so the cash is simply there when the bill arrives. The month our car needed four new tires, we had the money sitting there waiting. No panic, no credit card, no argument at the kitchen table. A few years earlier that same bill would have wrecked us. The only thing that changed was a habit I almost didn't bother starting: sinking funds.

If you have ever been blindsided by a bill you knew was coming, the car registration, the holidays, the insurance premium that lands as one big hit, this is the fix. It is calmer than it sounds, and once you set it up, most of the work disappears. Below are the sinking fund categories worth having, real examples of how much to set aside for each, and the small habit that makes it all run on its own.

Key takeaways

- A sinking fund is money you set aside a little at a time for a known, planned expense, so it is simply there when the bill arrives.

- The categories that help most are the big, irregular costs that wreck a normal monthly budget: car, insurance, holidays, home, and medical.

- To find your monthly amount, take the total cost and divide by the number of months until you need it. That is the whole math.

- You do not need a separate bank account for every fund. You need a list and a place to track it.

What a sinking fund actually is

A sinking fund is just deciding ahead of time. You take an expense you know is coming, divide it into small monthly amounts, and set that money aside until the bill shows up. It is simpler than it sounds. You are not investing, you are not budgeting harder, you are just spreading one painful payment across the calmer months before it.

Sinking fund vs emergency fund. People mix these up, so here is the clean line: an emergency fund is for the things you cannot see coming (a job loss, a surprise medical bill). A sinking fund is for the things you absolutely can see coming (the holidays in December, the car insurance in March). You want both, and keeping them separate is what stops you from raiding your emergency fund for Christmas.

The sinking fund categories worth having

You do not need all of these. Start with the three or four that have hurt you before. Here are the common ones, grouped, with an example monthly amount so you can see how small the pieces get. (These are illustrative examples, not a recommendation for your situation, your real numbers go in your own sheet.)

| Category | Example monthly | Frequency |

|---|---|---|

| Car maintenance and repairs (tires, brakes, oil) | $50/mo | Irregular, throughout the year |

| Car registration and inspection | $15/mo | Annual |

| Next car / replacement fund | $150/mo | Long-term, every several years |

| Car insurance (if you pay every 6 or 12 months) | $90/mo | Every 6 or 12 months |

| Property tax (if it is not in your mortgage) | $200/mo | Once or twice a year |

| Life or other annual premiums | $25/mo | Annual |

| Home maintenance and repairs | $100/mo | Irregular, throughout the year |

| Appliance replacement | $30/mo | Long-term, as things wear out |

| HOA or annual dues | $40/mo | Annual (or monthly) |

| Holidays and Christmas | $75/mo | Annual (December) |

| Birthdays and gifts | $30/mo | Throughout the year |

| Back-to-school | $25/mo | Annual (late summer) |

| Vacation | $100/mo | Annual or seasonal |

| Medical and dental (deductibles, the appointments you delay) | $50/mo | Irregular, throughout the year |

| Pet care (vet, annual shots) | $25/mo | Annual, plus surprises |

| Annual subscriptions and memberships | $15/mo | Annual |

How to set one up, in four steps

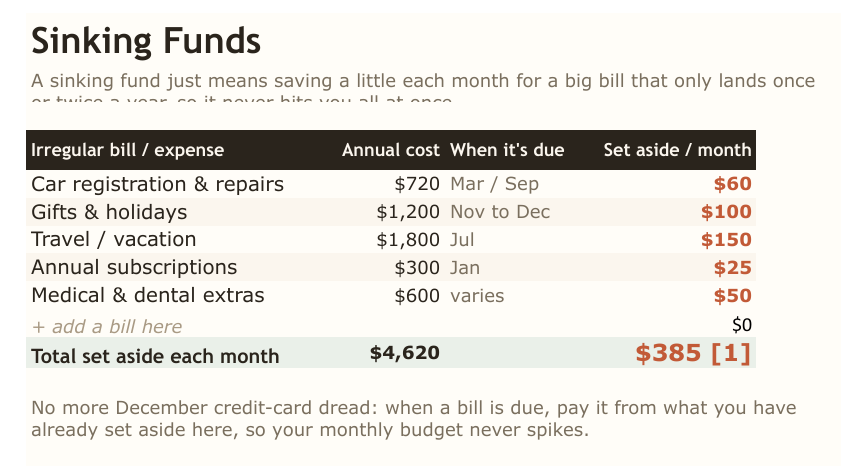

- List your known irregular bills for the next 12 months. Walk through last year's statements. The forgotten ones (registration, the vet, that annual app renewal) are exactly the ones that ambush you.

- Write the total cost and the date you need it next to each one.

- Divide the total by the months until it is due. That is your monthly amount. A $1,200 car insurance bill due in 12 months is $100 a month. That is the entire calculation.

- Set that money aside every month and track the balance so you can see it growing toward each bill. This is the part that, in our sheet, happens on its own.

This is the part the free starter sheet handles for you. You type the bill, the total, and the date, and it works out the monthly amount and tracks the running balance. No formulas to write, no math to redo when a number changes.

What tripped me up

I overdid it the first time. I made eleven sinking funds in one weekend, felt very organized, and quietly abandoned half of them by spring because I could not fund them all. The version that finally stuck was four categories, not eleven: car, insurance, holidays, and home. Start small. You can always add one later.

The other common mistake is keeping the money so accessible that it quietly leaks into everyday spending. You do not need a bank account for each fund, but you do need to track each balance separately, on paper, in a sheet, wherever, so a holiday fund and a car fund never blur into one pile you dip into without noticing.

free download

Get the free Sinking Funds Tracker

I built a free starter version of the exact sheet I use with my own family. You list your bills, it works out the monthly amount for each, and it tracks the balances so nothing sneaks up on you. Tell me where to send it and it is yours.

When you want the whole system

The free tracker covers sinking funds. If you want them wired into your whole year, so the amount you set aside flows straight into a budget that also forecasts which months will run tight, that is what the northcell Annual Budget does. Its sinking-fund auto-funder is the same idea as above, working alongside a full 12-month dashboard. Same calm, more of your money in one view.

Frequently asked questions

How many sinking funds should I have?

As few as you can get away with. Start with the three or four categories that have actually hurt you, and add more only when funding them feels easy.

Where should I keep the money?

Wherever you will not accidentally spend it. A separate savings account is tidy, but one account with the balances tracked separately works just as well. The tracking matters more than the number of accounts.

Sinking fund vs emergency fund, which first?

Build a small emergency starter fund first so a true surprise does not derail you, then layer sinking funds on top for the bills you can see coming.

What if I cannot fund all my categories yet?

Fund the most urgent ones fully before adding more. A fully funded car-repair category beats five half-funded ones you cannot rely on.

Do I need a separate bank account for each one?

No. You need a list and a place to see each balance. That is the whole job.

Related reading

Designed and written by northcell. For organization and planning purposes only, not financial, tax, or legal advice. Our tools and guides are original works created with AI-assisted design; every formula is human-tested and verified.